- May 29, 2025

- 10 min read

Updated: Nov 6, 2025

Key Points

Pet insurance helps you pay for unexpected accidents and illnesses by reimbursing you for a portion of eligible vet bills.

The best pet insurance plans can cover up to 90% of eligible vet bills, which can include costs for surgery, diagnostic testing, cancer treatment, and hereditary conditions.

Enrolling in pet insurance early and choosing the right insurance plan can help you maximize your coverage and other benefits.

Pet insurance can be worth the cost if you select a plan that has the right amount of coverage for your pet.

Some pet parents and pet websites say that it can be a smart way to protect your wallet –– and that’s true. However, at Pumpkin, we believe the most important benefit of pet insurance is that it helps you say ‘yes’ to the best treatment for your pet, ensuring that care decisions don’t turn into cost decisions.

It’s important to note that pet insurance doesn’t work the same way as human health insurance, but the right amount of coverage can take the stress out of vet visits and emergency care when your pet is hurt or sick. Being able to focus on your pet’s recovery and worry less about the cost can provide priceless peace of mind for many pet parents. Continue reading to find out if pet insurance is worth it for you and your pet.

How is Pet Insurance Different?

Most pet insurance plans, including Pumpkin Pet Insurance, work on a reimbursement model. This is typically how pet insurance works: Instead of the veterinary clinic billing the insurance company directly, you’ll pay the vet bill upfront. Afterwards, you submit a claim, and your pet insurance can reimburse you for up to 90% of the eligible vet bill cost.

Without pet insurance, you are responsible for paying that full vet bill on your own. A recent Gallup and PetSmart Charities survey revealed that 71% of pet parents avoided going to the vet because they were concerned about the cost. If you are trying to save money, large unexpected vet bills can drain your bank account or put you into debt. This shouldn’t be on your mind while choosing care for your pet, and that is the biggest benefit of pet insurance.

So, is pet insurance worth the cost? Thousands of Pumpkin Pet Insurance pet parents certainly think so. And if you’re considering enrolling your dog or cat in a pet insurance plan, whether with Pumpkin or not, we want to give you all the info you need to make an informed choice. Keep reading to discover all the ways pet insurance can help you protect your pets and your savings in the process.

Can Pet Insurance Save You Money?

In the long-run, pet insurance could help save you from having to drain your savings account for an unexpected pet accident or illness. We don’t like to think about the worst case scenario with our pets, but it can happen. Some breeds are even predisposed to certain conditions, so it’s a good idea to have pet insurance as a tool in your arsenal.

Pet insurance has helped countless pet parents get back thousands of dollars on life-changing treatment over the course of their pets’ lives. Precisely how much money pet insurance reimburses can depend on how much treatment your dog or cat receives, how long you’re enrolled in a pet insurance plan, and what coverage features you choose, such as your plan’s annual limit.

So, if your Pug is enrolled in a plan with a $10,000 annual limit, you could get up to $10,000 back with every year of coverage — though, in all likelihood, your pet won’t need that much treatment every single year. If your Pug jumps off the couch and needs x-rays and surgery to repair a broken bone, having a high or unlimited annual limit might come in handy. With pet insurance plans from Pumpkin, parents can choose annual limits from $5,000 all the way up to unlimited. They can also choose an 80% or 90% reimbursement rate, and an annual deductible as low as $100 or as high as $1,000.

Let’s explore a real-life example from a Pumpkin pet named Argus.

"Argus managed to swallow rocks on four different occasions as a puppy. He had four surgeries. Our Pumpkin insurance plan helped cover all of them without question. Argus is now three years old, healthy, and no longer swallows rocks."

– JoAnn, Argus's Parent

Argus was just a puppy, and already JoAnn had to pay more than $12,000 for four separate surgeries. Her pet insurance plan reimbursed her for 90% of the eligible bills after meeting her annual deductible, resulting in $10,644.37 in cash back. A 90% reimbursement rate and a high $15,000, $20,000, or unlimited annual limit can make financial sense for pet owners who want to maximize their cash back but are concerned their pets could have multiple accidents or illnesses in a given year.

Why invest in pet insurance?

About 1 in 3 pets will need emergency vet treatment this year. Based on claims filed by Pumpkin pet parents between February 2022-2025, the average emergency vet bill for dogs costs $653. For cats, the average is $919. And those are just the averages; emergency vet treatment can cost a lot more.

As we’ve seen, unless you have a $12,000 emergency savings account or high-limit credit card for vet care, pet insurance can be a financial lifesaver. Pet insurance is a type of accident & illness coverage that can provide a safety net if your kitty or pooch gets hurt, injured, or sick unexpectedly. When you know that you can be reimbursed for up to 90% of your pet’s covered vet bills, it’s easier to get them the care they need.

How is pet insurance different from human health insurance?

Pet insurance functions like property and casualty insurance rather than human health insurance. You still pay the vet upfront as usual, and then you submit a claim and any necessary supporting documentation to your insurance provider. It’s similar to filing a claim for repairs after a car accident. With human health insurance, you usually pay a copay upfront, and the provider bills the insurance company directly.

Most pet insurance plans include 50-90% reimbursement rates. This means you can choose, once your deductible is met, whether you want 90% cash back on eligible vet bills, or less. A deductible is the amount you pay out of pocket before your claims will be eligible for reimbursement. While some pet insurance plans have a deductible for each new condition that develops, most plans –– including Pumpkin’s –– have one set annual deductible amount you must meet each year, no matter how many new conditions occur.

When buying a pet insurance plan, you will see something called an insurance premium, which is a monthly fee you pay to have insurance coverage. Insurance premiums vary in cost depending on the age, breed, zip code, and type of pet, as well as the deductible amount, reimbursement rate, and annual limit.

On top of this, pet insurance comes in a variety of types. There are accident-only plans, which only cover claims for accidents OR accident and illness plans that cover both accidents and illnesses. All pet insurance plans from Pumpkin are accident and illness plans, and they cover a variety of treatments and tests.

All of these elements change how much you pay each month for pet insurance. We recommend getting a pet insurance quote with any provider you are considering to see exactly what will be covered and the options available to customize your plan.

What are pet wellness plans?

Pet insurance plans protect you and your pet from unexpected accidents and illnesses in the future. So, while your own health insurance may cover preventive and routine care, that’s not the case with pet insurance plans. Likewise, pet insurance plans typically don’t cover pre-existing conditions.

If you’re interested in getting help paying for routine vet care like annual wellness visits, vaccinations or flea and tick prevention, you may want to consider an add-on or separate pet wellness plan. Depending on the provider you choose, wellness plans can either be insurance benefits or non-insurance benefits. While not all insurance providers offer wellness plans –– and state availability varies –– you can find out by visiting a provider’s website.

What does pet insurance cover?

Pet insurance policies differ widely in cost and coverage. Basic insurance plans may be accident-only policies, but most providers offer accident & illness coverage as well. Pet insurance plans could help you pay for a wide range of diagnostics and treatments for accidents and health problems, including hereditary conditions, dental illnesses, and even behavioral issues.

Let’s get more specific. If you enroll your pet in a Pumpkin Pet Insurance plan, you can get help paying for eligible vet bills for accidents such as:

Injuries like bite wounds or hot spots

Orthopedic injuries like fractures

Swallowed objects like toys, socks, rocks, sticks, and more

Ingested toxins, like poisonous plants or toxic foods such as chocolate

Examples of illnesses:

Parasite infections and diseases

Skin infections and diseases

Respiratory illnesses like kennel cough

Digestive illnesses

Ear infections

Cancer

Hip Dysplasia

Dental diseases, like gum disease

Preventable illnesses, like Lyme disease

Examples of Eligible Test and Treatment Expenses:

Bloodwork

X-Rays

Ultrasounds, CT scans and MRIs

Prescription Medications

Prescription Food or Supplements

Emergency Care and Hospitalization

Advanced or Specialized Care, Including Chemotherapy and Stem Cell Therapy

Surgeries and Non-surgical Procedures

Behavioral Therapy

Of course, each claim is unique, and these are just examples. You’ll likely need to meet a deductible before you can be reimbursed for eligible veterinary costs.

What does pet insurance not cover?

Designed to cover accidents and illnesses, standard pet insurance plans don’t usually cover routine or preventive care. So, annual vaccines or checkups are generally excluded.

These are common exclusions you’ll find in most pet insurance plans:

Pre-existing conditions

Grooming and cleaning services

Pet boarding and travel costs

Cosmetic or elective procedures

Spay/neuter procedures

Pregnancy care and C-sections

It’s always a good idea to read the fine print of any pet insurance policy you’re considering, so you’re not caught off guard by surprises when your pet needs advanced or emergency care.

Tips for Buying Pet Insurance

Buying pet insurance can help pet parents plan ahead. Here are some tips to make the most of this investment.

Start early

Is pet insurance worth it for a puppy or kitten? Ultimately, that’s a call you’ll have to make, but there are huge benefits to enrolling early.

Since pet insurance excludes pre-existing conditions, the longer you wait to enroll, the more potential exclusions your pet will face. By enrolling your pet in a plan when they’re young and healthy, you’ll maximize their potential coverage throughout their life.

Plus, you’ll have peace of mind knowing you have financial support to help cover costs when your puppy or kitten decides to get into the most expensive trouble possible.

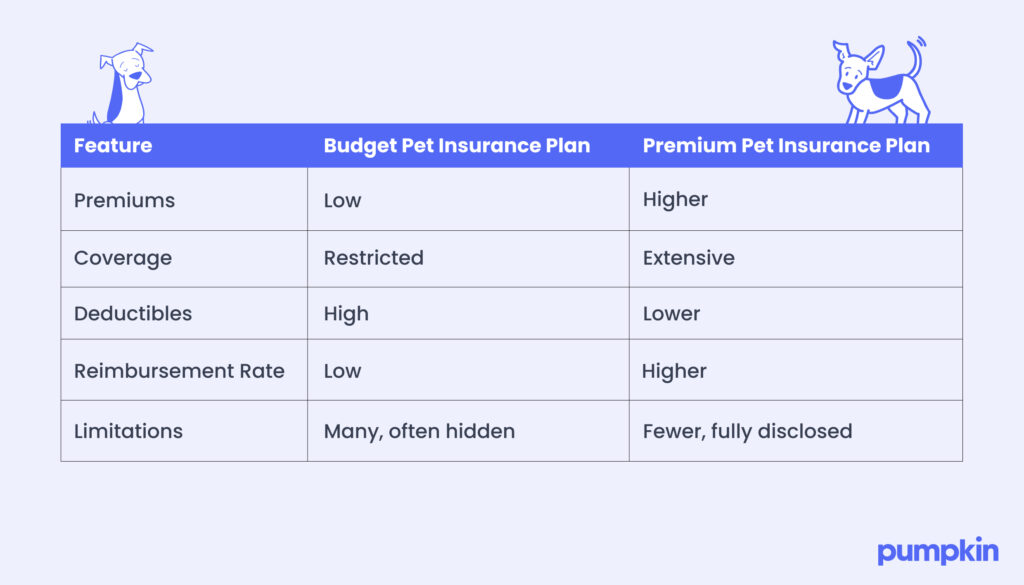

Remember: cheap pet insurance can cost more

When it comes to the cost of pet insurance, choosing your policy based solely on the lowest premium is a risky strategy.

Cheap monthly rates or premiums sound great, but they usually come with higher deductibles, longer waiting periods, lower annual limits and reimbursement rates, and possible exclusions or add-on fees for common conditions and treatments. That means a “budget” pet insurance plan could end up costing you more in the long run.

Let’s say your Golden Retriever puppy breaks a leg during your insurance plan’s extended waiting period of 180 days. You’ll have to pay the entire bill alone, on top of the regular monthly premiums. Low-cost pet insurance plans typically have a 50% to 70% reimbursement rate, an annual limit lower than $5,000, and high deductibles, which can leave you on the hook for thousands of dollars in emergency vet bills.

With Pumpkin’s pet insurance plans, all pet parents have the option to get up to 90% cash backon eligible vet bills. Some plans have deductibles as low as $100. You can also choose from flexible annual limits, including unlimited plans.

If you want more protection for a particularly adventurous pet, choosing an extensive plan with higher payments may be the smart choice. While you will have to pay higher monthly premiums, your deductible and max out-of-pocket costs may be significantly lower.

Compare different pet insurance plans to see how much more coverage you can get with a more extensive plan.

Read the fine print

Always, always, always read a sample policy document carefully before you commit. You never want to discover your insurance doesn’t cover the procedure your pet needs the most. Pay attention to what is and isn't covered, mandatory waiting periods, exclusions, and limitations.

Some pet insurance companies also have age restrictions and may decline to insure older pets or reduce coverage as your pet ages.

Pumpkin takes a different approach. There are no upper age limits for enrollment and no reduced coverage as your pup or cat ages — so rest assured you can provide the best care for your pet as they enter their golden years.

Appeal denied claims

Sometimes, pet insurance claims can be denied. Fortunately, most pet insurance companies have an appeals process, and you might be able to file an appeal to get reimbursed. So don't give up right away; contact your insurance provider for more information.

So is pet insurance worth the cost?

Still wondering, “Should I get pet insurance?” Clearly, many pet parents say yes. In fact, a recent survey by the credit monitoring agency Experian found that 92% of pet owners with insurance said that they believe their pet insurance is worth it. And every year, the North American Pet Health Insurance Association (NAPHIA) reports thousands more pets are enrolled in pet insurance plans, which is why the industry is growing so quickly.

Hopefully, you now have the info you need to make the right decision for your pet. Stressing about whether you can afford veterinary care shouldn’t be a part of the pet parenting journey. Pet insurance can make the unexpected turns a little easier by helping you say "yes" to the best care, even when it comes at a high cost.

Interested in learning more, or seeing how much pet insurance will cost for your favorite dog or cat? Fetch a free quote from Pumpkin now.

FAQs

Is it too late to sign up for pet insurance?

It’s never too late! Even if your pet is already sick or diagnosed with an illness, pet insurance can still be helpful. While it won’t cover the treatment costs for that specific condition (those are considered pre-existing), it can still cover future illnesses and accidents.Senior dogs can also have lots of health complications, making pet insurance helpful for their parents. Luckily, Pumpkin doesn’t discriminate based on age. So, even if your furry friend is rocking some grey hair, you can still sign up.

Should I get pet insurance for a purebred dog?

As much as we love our Frenchie friends and fluffy Chow Chows, some purebred dogs can face more health challenges than mixed-breed pets. If you’re worried about paying for vet care over your pet’s lifetime, then it’s important to have a plan. A pet insurance plan can put your mind at ease if your pooch needs to see the vet for an unexpected accident or illness. To support our purebred pups, Pumpkin Dog Insurance plans don’t exclude hereditary conditions or charge extra for breed-specific health issues.

A Pumpkin Pet Insurance plan covers prescription food & supplements to treat an eligible accident or illness. It does not cover prescription food & supplements used for weight management or general health maintenance.